Last updated: Feburary 12, 2024

EFRAG recently published the draft of the voluntary ESRS (European Sustainability Reporting Standards) for small and medium-sized enterprises. These standards are designed to encourage micro, small and medium-sized enterprises to contribute to a more sustainable and inclusive economy.

They aim to improve their management of sustainability issues such as pollution, health and safety of employees – issues they face on a daily basis. The standards are also intended to facilitate access to finance and meet the requirements of larger companies in the value chain.

This article explains who exactly is affected, how the standards are structured and what first steps affected companies should take now.

Inhaltsverzeichnis

- What are the VSME ESRS?

- Who should & should not report VSME?

- How are the VSME structured?

- How does Code Gaia implement the VSME?

- Deciding what to report & first steps for companies

1. What are the VSME ESRS?

VSME ESRS (“the VSME”) is abbreviated from “Voluntary Small and Medium Enterprise European Sustainability Reporting Standard” and is the sustainability reporting standard which is recommended for micro, small and medium companies who operate within the European Union to adopt on a voluntary basis. Use of the VSME should be considered by any European company which is not compelled to report by regulation.

In the words of EFRAG, the VSME is “intended to be a simple reporting tool to assist non-listed micro-, small- and medium-sized enterprises (non-listed SMEs) in responding to requests for sustainability information that they receive from business counterparts (i.e., banks, investors or larger companies for which non-listed SMEs are suppliers) in an efficient and proportionate manner as well as to facilitate their participation in the transition to a sustainable economy.

The VSME is expected to “standardise the current multiple ESG data requests (which represent a significant burden on non-listed SMEs), by reducing the number of uncoordinated requests they receive. This is expected to support them in having better access to lenders, investors and clients.”

As at January 2024, the VSME standard is still an “Exposure Draft”. This means that the standard is still undergoing exposure to comment and consultation from the market with regards to its content. According to EFRAG, “the consultation period will run until 21 May 2024, and EFRAG invites all stakeholders to provide comments through the online consultation questionnaires.” We expect an official release of the standard later in the year.

2. Who should & should not report VSME

Companies who are required under the CSRD to prepare a “Sustainability Statement” in compliance with the ESRS should not be adopting the Voluntary Standard. The Voluntary Standard is intended for companies which are “micro” enterprises and those which are Small and Medium Enterprises, but which are (1) not listed on any European stock exchange or (2) also are not Public Interest Entities. The definitions of these entities are found in the Accounting Directive. Sustainability and reporting professionals should familiarise themselves with the Accounting Directive, or at least confer with their accounting functions to clarify.

In December 2023 another standard, the ESRS for Listed SMEs (ESRS LSME), was announced. The LSME is targeted at Small and Medium Enterprises that are listed on a European stock exchange and thus required to report sustainability information in accordance with the Accounting Directive. More information regarding the form and content of the LSME standard is expected later in 2024.

3. How are the VSME structured?

The VSME standards follows a very simple structure of three modules:

- Basic Module

- Narrative: Policies, Actions, and Targets (PAT) Module

- Business Partners (BP) Module

This modular approach to reporting allows for SMEs of all sizes and avoids overwhelming smaller companies with little to no formalised processes of sustainability reporting.

- The Basic Module consists of 12 disclosure requirements and asks for a standard set of metrics in the categories Environment, Social matters, and Business Conduct. The metrics are a stripped down version of the disclosure requirements of the full ESRS. This module is the minimum requirement to be fulfilled by all reporting companies.

- The Narrative: Policies, Actions, and Targets Module consists of 5 disclosure requirements of a qualitative nature. It aims to provide the information necessary to understand how a company manages different sustainability matters.

- The Business Partners Module is designed to support the SME in collecting datapoints relevant for business partners, investors, and lenders. These 11 disclosure requirements are additional to information in the previous two modules and contain a mix of quantitative and qualitative requirements.

While the Basic Module is simply a collection of metrics and can be easily adopted even by micro and small enterprises, the other two modules require the completion of a materiality assessment beforehand. This will help the company to identify which topics are relevant to them and thus need to be reported on.

4. How does Code Gaia implement the VSME?

Code Gaia has already implemented the draft VSME standard into our software in order to allow companies to accustom to the standard early on. The content will be updated after the official release of the standard later in the year.

To make the reporting process as easy as possible the content of the VSME standard has been broken down in the Code Gaia framework into 5 sections.

- Sections 1 and 2 are derived from the Basic Module. The first section of just two requirements covers the general content relating to reporting scope and approach. The second section breaks down the 10 metric requirements into single data points.

- Section 3 is an additional, optional section which allows for a description of any materiality-based process which has been used to set the scope of the PAT and BP Modules (sections 4 and 5 of the Code Gaia framework). Use of section 3 to report the process of materiality analysis is optional but recommended for more transparency.

- Section 4 contains the requirements of the Narrative: Policies, Actions, and Targets Module. These requirements are largely qualitative in nature and require the explanation of internal sustainability measures.

- Section 5 contains the requirements of the Business Partners Module. As with section 4, these requirements are subject to a company’s own materiality analysis and disclosures are simply omitted if they are found to be not material.

The diagram below illustrates how the VSME Modules have been incorporated into the 5 framework-sections in the Code Gaia reporting software

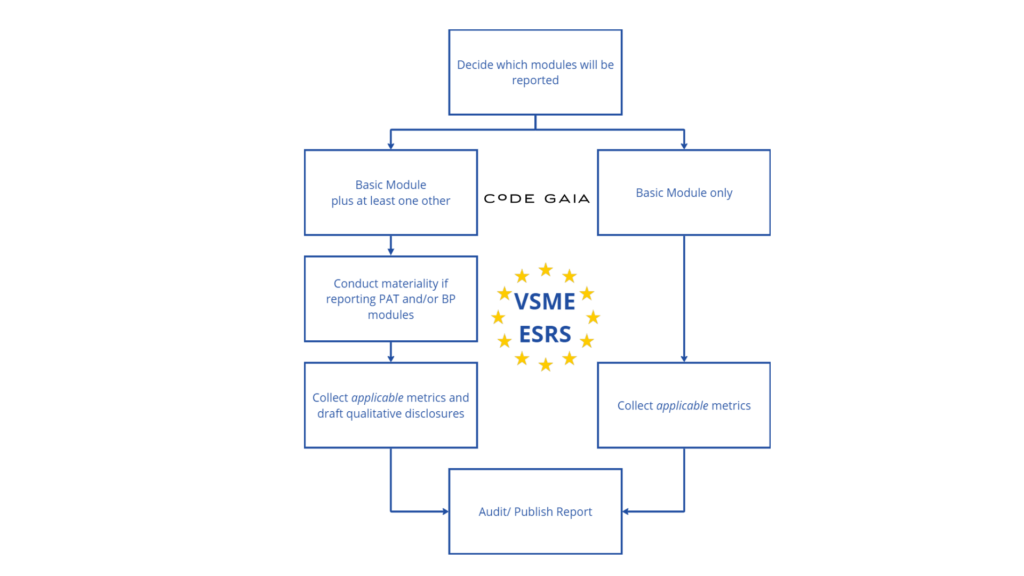

5. Deciding what to report & first steps for companies

Despite being in draft form, the VSME standard can already serve as a suitable vehicle for collecting and reporting sustainability information in a way that is explicitly tailored to smaller businesses in Europe.

Unlike the full ESRS, the scope of VSME reporting is not explicitly determined by company size, sector or a materiality process. Rather, a decision regarding which modules are practicable or reasonable should first be made by the reporting company.

Whilst the Basic Module should be reported by all VSME-reporting entities and is seen as a prerequisite for applying further modules, the PAT and BP modules are reported subject to their applicability and materiality. According to the standard, the PAT module “is suggested to undertakings that have formalised and implemented PAT”. Companies with only ad.hoc. approaches to sustainability Policy, Actions and Target setting would likely scope-out this Module. This means that considerable report scoping and streamlining can occur prior to any decision to undertake materiality assessment.

Code Gaia considers that a review of the three modules should take place early in the reporting process, and that a decision regarding which of the two optional modules are relevant should be made. Once this decision is made, the scope and process of reporting will be clear.

In summary, the VSME ESRS provide small and medium-sized enterprises in the EU with a clear guide to sustainability reporting.

With a simple, modular approach, they allow for a step-by-step implementation, while a smart choice of modules minimizes the reporting burden.

The standards, which are currently in draft form, are expected to be published later this year. Code Gaia has already started to integrate the VSME into its software to allow companies to adapt early.