How process descriptions work in the ESRS (European Sustainability Reporting Standard)

In this article, I take a look at how the ESRS sets the requirements for reporting various sustainability process disclosures. In particular, I will be using example requirements from the Climate Change Standard, ESRS E1.

The summary take-away of this is to understand that the ESRS often contains many prescriptive looking sections and references to externally established processes. However, reporters should be aware that the focus of the ESRS is process transparency, and not prescription. This means that disclosing that a specific process was not carried out is sufficient for the purposes of compliant information disclosure.

Transparency, not prescription

The ESRS’s requirement for a description of the processes to identify and assess material climate-related impacts, risks and opportunities comes from the cross-cutting requirements of the General Disclosures standard (ESRS 2). Within each topical standard, a matching requirement (repeated, similar to how the GRI uses per-topic management approach disclosures) asks for that topic’s relevant process. Within the Climate change standard (E1) this is the fourth Disclosure Requirement (E1-IRO-1 in Code Gaia software).

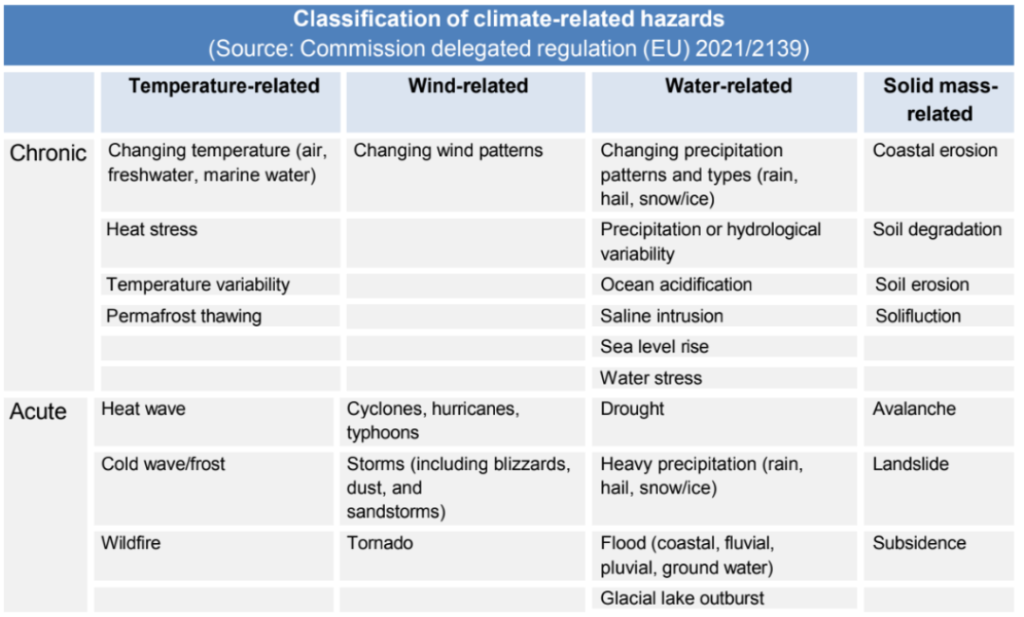

When disclosing information about physical climate related risks, ESRS E1 expects companies to clarify whether their processes to identify and assess physical risks took account of specific “climate related hazards”. This requirement comes from ESRS E1 (Climate change) AR 11.

The specific list of climate hazards is found within Commission delegated regulation (EU) 2021/2139, which is part of the regulations which make up the EU taxonomy for sustainable activities. It makes sense therefore, that companies who also report EU-taxonomy related disclosures also provide adequate information in accordance with ESRS E1 AR 11.

For those companies which are not reporting also under the taxonomy it would be sufficient to state that these hazards have not been systematically considered, or, that they have been taken into account in an ad.hoc. manner outside the taxonomy process. In other cases, companies may wish to adopt the taxonomy hazard classification, even if they are not required to report under the taxonomy.

As is typical for the ESRS, the requirement here is one of process transparency. The ESRS does not prescribe the use of these hazards, but does expect transparency with respect or whether they have been taken into account.

Source ESRS E1 Application Requirement 11

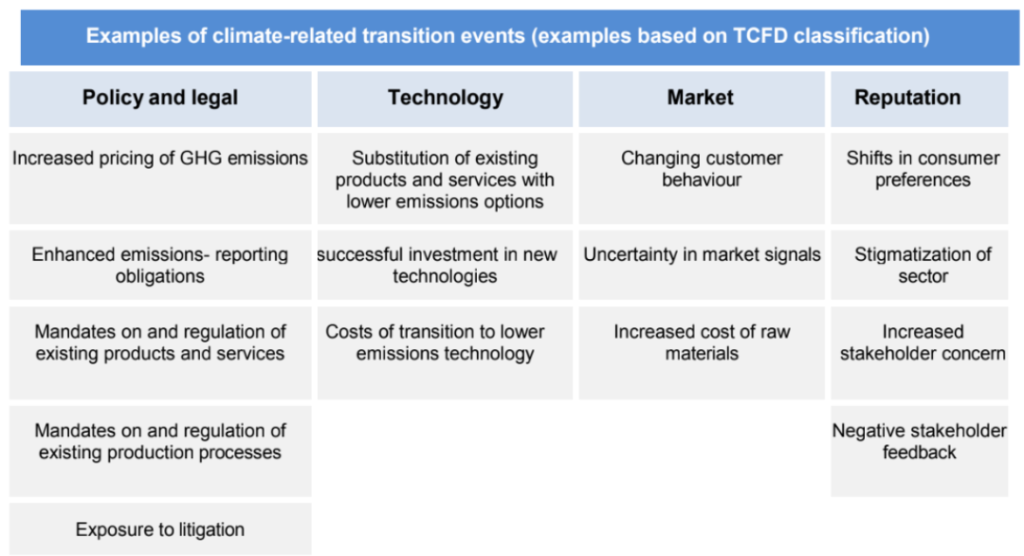

Similar to the requirements specified in AR11, AR12 also expects transparency with respect to the identification of “transition events”. The requirement is that reporting companies are to “explain whether and how it has identified transition events over the short-, medium- and long-term and screened whether its assets and business activities may be exposed to these events.”

A specific tabulated list of the “transition events” is provided in ESRS E1, which is reproduced below.

Once again, the ESRS is concerned with process transparency and does not prescribe the use of these as a pre-requisites for CSRD/ESRS compliance. A compliant sustainability statement should indicate whether these transition events have been used in the relevant decision-making process.

ESRS E1 AR 11, S. 94

Improved transparency as primary objective

Whilst the requirements of the ESRS are convoluted and can appear overwhelming at first glance, it is important to note that one of the primary objectives of the CSRD is improved transparency. Stating that a specific process or classification system was not taken into account is, in this context, compliant.

Reporting companies need not achieve full process alignment in order to report. In fact, a staged adoption of process improvement when it comes to sustainability management can follow after reporting.